On a weekly basis I share 4 charts/tables that I find interesting. I hope you find them educational. Please feel free to share or respond if you want to dig deeper on a particular topic. As always, nothing here is a recommendation.

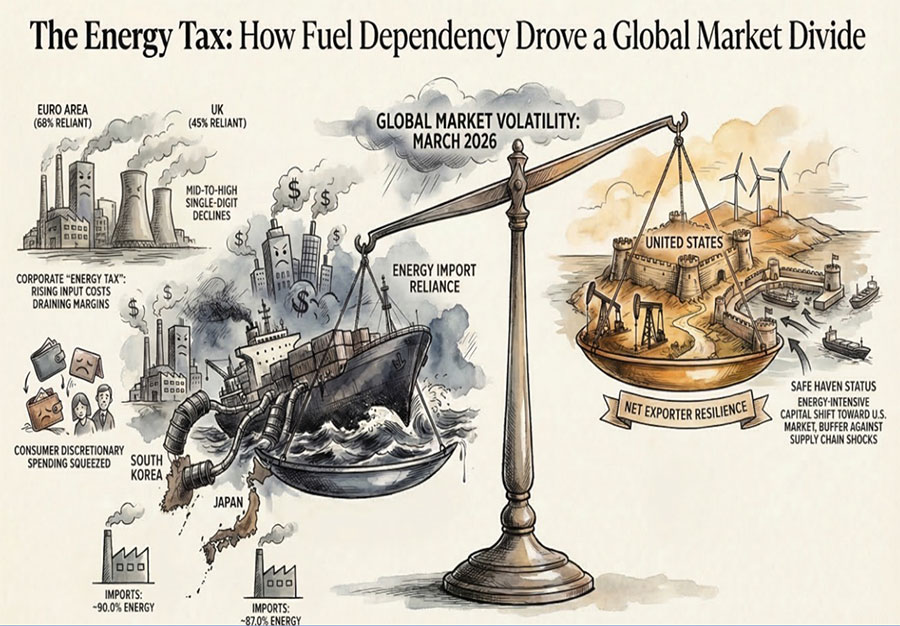

The recent surge in global energy prices has provided a masterclass in financial resilience. While headlines often focus on the conflict itself, the real story for investors is the stark divergence in how different economies and asset classes are responding. From the “energy tax” impacting import-dependent nations to the surprising shift in traditional “safe haven” assets, the market is currently defying historical patterns. In this week’s charts, we break down why the U.S. remains a relative anchor of stability and what the $100-per-barrel oil threshold means for inflation and your borrowing costs.

Key Takeaways:

The Energy Divide: Japan and South Korea saw double-digit or near-double-digit equity plunges due to energy import reliance, while the S&P 500 remained resilient with only a 3.0% decline.

The Stagflation Threat: Rising oil prices increase the probability of “Quad 3″—a regime of decelerating growth paired with accelerating inflation.

The Debt Factor: With national debt approaching $40 trillion and war-related spending rising, the Treasury is forced to offer higher yields to attract buyers, keeping borrowing costs elevated for everyone.